Imagine you are the first generic drug company to challenge a blockbuster medication's patent. You spend millions on legal fees and regulatory paperwork. You win. The law grants you a 180-day head start with no other generic competition. This is your reward for taking the risk. But then, right before you launch, the original brand-name company releases its own "generic" version of the drug. It costs less than their brand but more than yours. Your exclusive window just got crowded. Your profits take a massive hit. This is the reality of authorized generics in the world of pharmaceutical patent litigation.

What Are Authorized Generics?

To understand the controversy, we need to define what an authorized generic actually is. It is not a traditional generic drug made by a different manufacturer using their own facilities. Instead, it is the exact same product as the brand-name drug, produced by the original pharmaceutical company or a licensee they approve. They simply repackage it and sell it under a generic name.

Authorized Generic is a branded pharmaceutical product marketed under a generic label by the original manufacturer or a licensed partner, requiring no new FDA clinical approval.

Because the product is identical to the brand-name version, the Food and Drug Administration (FDA) does not require new safety or efficacy testing. The manufacturer files a supplemental application to the existing New Drug Application (NDA). This allows them to bypass the lengthy and expensive process that independent generic manufacturers must go through. They can enter the market quickly, often within weeks of a court ruling or patent expiration.

The legal foundation for this practice comes from the Hatch-Waxman Act of 1984. Also known as the Drug Price Competition and Patent Term Restoration Act, it established the framework for generic drug approval in the United States. While the act grants 180-day marketing exclusivity to the first generic competitor who successfully challenges a patent via an Abbreviated New Drug Application (ANDA), it does not explicitly prohibit the brand owner from selling their own generic version during that period. The FDA has consistently ruled that this is permissible, creating a legal gray area that fuels ongoing debate.

The Mechanics of Market Entry

How do these drugs appear so fast? Independent generic companies must file a Paragraph IV certification, stating that the brand’s patents are invalid or will not be infringed. This triggers a lawsuit. If the generic wins, they get the 180-day exclusivity. Authorized generics skip this entire battle. They rely on the brand’s existing regulatory approval.

Data from Lex Machina’s 2022 patent litigation database reveals a striking pattern: 73% of authorized generics enter the market within one week of a court ruling against the branded company’s patent. This speed is a strategic weapon. By launching immediately, the brand company prevents the independent generic from capturing the full value of their exclusivity period.

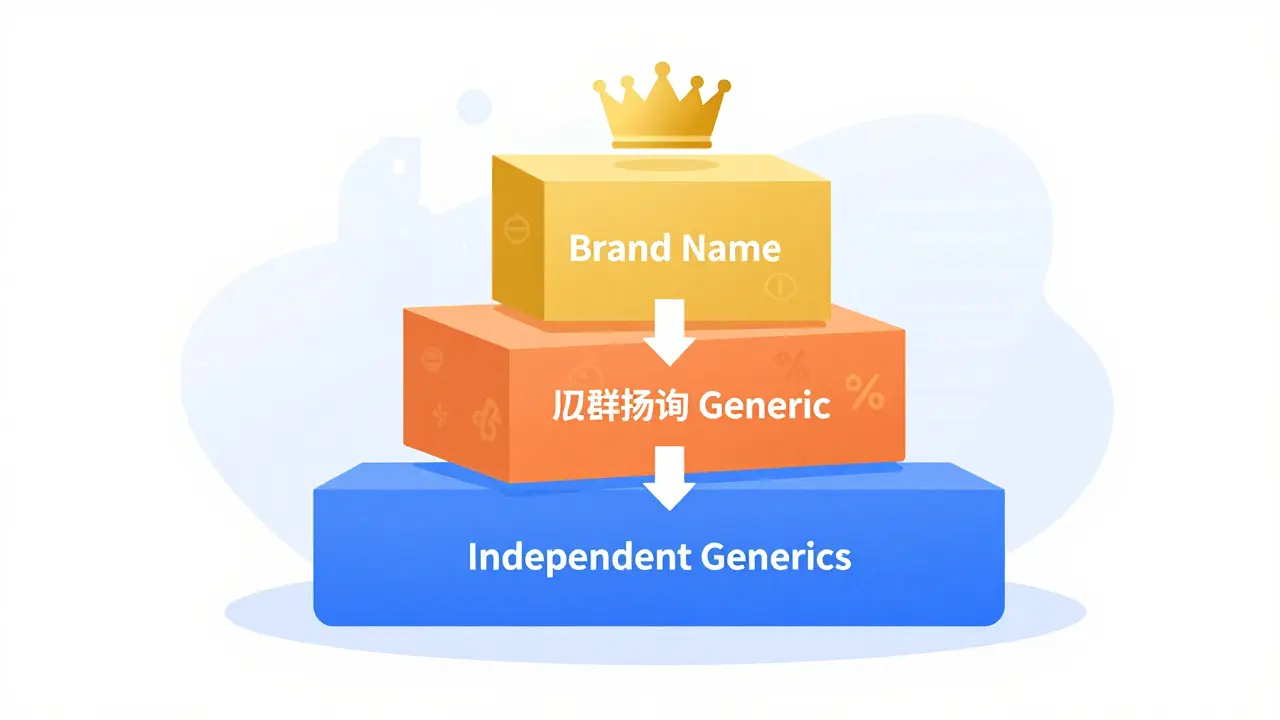

The pricing strategy is equally calculated. Authorized generics typically launch at a price point between the brand and the independent generic. For example, if the brand costs $100, the authorized generic might cost $85, while the independent generic aims for $50. This creates a three-tiered market:

- Brand Name: Highest price, covered by most insurance plans without restriction.

- Authorized Generic: Mid-tier price, often preferred by Pharmacy Benefit Managers (PBMs) looking for savings without switching formularies entirely.

- Independent Generic: Lowest price, but now facing immediate competition from the mid-tier option.

This structure segments the market. Patients and insurers who want some savings but trust the brand manufacturer flock to the authorized generic. The independent generic, which expected a monopoly for six months, suddenly has to fight for share against a product with the same quality assurance as the brand.

Impact on Competition and Revenue

The economic impact of authorized generics is severe for the first-filing generic companies. The Federal Trade Commission (FTC) conducted a comprehensive analysis in their 2011 report, "Authorized Generic Drugs: Short-Term Effects and Long-Term Impact." The findings were stark.

When an authorized generic enters the market during the 180-day exclusivity period, it captures between 25% and 35% of the market share. This directly reduces the revenues of the first-filer generic by 40% to 52%. The damage doesn't stop when the exclusivity period ends. In the subsequent 30 months, first-filer generics face 53% to 62% lower revenues compared to scenarios where no authorized generic was present.

| Scenario | Market Share Capture | Revenue Reduction for First-Filer |

|---|---|---|

| No Authorized Generic | Generic captures 80-90% | N/A (Baseline) |

| With Authorized Generic (During Exclusivity) | AG captures 25-35% | 40-52% reduction |

| Post-Exclusivity (30 Months) | Continued Competition | 53-62% reduction |

Consider the case of Teva Pharmaceutical. In their 2018 annual report, they noted a $275 million revenue shortfall directly attributable to authorized generic competition for specific products. These aren't small numbers. They represent the profit margin that incentivizes generic companies to take on the legal risks of patent challenges in the first place.

Patent Settlements and Anti-Competitive Behavior

The most controversial aspect of authorized generics involves patent litigation settlements. When a brand company faces a patent challenge, they often settle rather than risk losing the patent in court. Historically, these settlements sometimes included "reverse payments," where the brand paid the generic to delay entry. While the Supreme Court ruled in FTC v. Actavis (2013) that such payments require antitrust scrutiny, a more subtle form emerged: agreements regarding authorized generics.

Data from fiscal years 2004-2010 showed that approximately 25% of patent settlements involving first-filing generics included explicit agreements where the brand committed not to launch an authorized generic. In exchange, the generic firm agreed to delay market entry. These arrangements resulted in average delays of 37.9 months beyond the original settlement date. Essentially, the brand bought off the generic competitor by promising not to use their most effective competitive weapon.

The FTC has labeled this behavior anti-competitive. Joseph Simons, former FTC Chairman, stated in 2019 congressional testimony that "reverse payment settlements involving authorized generics represent the most egregious form of anti-competitive behavior in the pharmaceutical sector." The logic is simple: if generics fear that winning a patent challenge will only lead to a price war with the brand’s own authorized generic, they may choose not to challenge the patent at all. This keeps prices high for consumers.

However, recent trends suggest a shift. A 2023 study published in the American Journal of Health-System Pharmacy found that authorized generics are significantly less likely to enter the market following a patent settlement today than they were in the past. This decline correlates with increased regulatory pressure. The FTC opened 17 investigations into potential anti-competitive authorized generic arrangements since 2020. The message to pharma companies is clear: using authorized generics as a bargaining chip in settlements is risky.

Stakeholder Perspectives: Who Wins and Who Loses?

The debate over authorized generics is not black and white. Different stakeholders view the practice through very different lenses.

Generic Manufacturers: Organizations like the Association for Accessible Medicines (formerly GPhA) strongly oppose authorized generics. Chip Davis, former CEO of GPhA, testified in 2015 that the practice "undermines the Hatch-Waxman Act by devaluing the 180-day exclusivity period incentive." Without the promise of exclusive profits, fewer generic companies will invest in challenging weak patents, ultimately hurting patient access to affordable drugs.

Branded Pharmaceutical Companies: Groups like PhRMA argue that authorized generics increase competition. They claim that providing an additional supply option lowers prices for pharmacies and patients. A 2022 white paper cited research showing that on-invoice prices for new generics were 13-18% lower when an authorized generic was available. From their perspective, they are simply offering consumers a choice.

Pharmacy Benefit Managers (PBMs): PBMs, which negotiate drug prices on behalf of insurance companies, generally support authorized generics. A 2023 survey by AIS Health found that 68% of PBM executives prefer formularies that include authorized generics. Why? Because it gives them another lever to pull when negotiating rebates. More suppliers mean more competition, which means better deals for the PBM.

Regulators: The Congressional Research Service maintains a nuanced position. While acknowledging the financial harm to first-filers, their 2006 analysis noted that the presence of authorized generics "has not substantially reduced the number of challenges to branded drug patents by generic firms." However, they did note that for smaller drugs with sales between $12 million and $27 million, the threat of an authorized generic could deter patent challenges entirely.

Current Trends and Future Outlook

As of 2026, the landscape of authorized generics is evolving. The prevalence of these launches has decreased. A 2023 study in JAMA Internal Medicine reported that authorized generic launches dropped from 42% of relevant markets in 2010 to 28% in 2022. Several factors drive this decline:

- Increased Scrutiny: The FTC’s 2022 Policy Statement on Pharmaceutical Competition explicitly targeted agreements that delay authorized generic entry. Holly Vedova, Director of the Competition Bureau, warned that the Commission would challenge any arrangement circumventing the Hatch-Waxman structure.

- Legislative Pressure: Senators Amy Klobuchar and Chuck Grassley have reintroduced the Preserve Access to Affordable Generics and Biosimilars Act multiple times. While it hasn’t passed yet, the persistent legislative effort signals that Congress is watching closely.

- Strategic Shifts: Branded companies are developing more sophisticated lifecycle management strategies. Rather than relying solely on authorized generics, they are exploring other avenues to extend market dominance, such as reformulations or new delivery mechanisms.

Despite the decline, authorized generics are not disappearing. Industry analysts at Evaluate Pharma project that they will continue to represent 20-25% of all generic drug entries through 2028. The key difference is how they are used. The era of using them as blunt instruments in anti-competitive settlements appears to be ending. Instead, they are becoming a standard, albeit contested, part of the competitive mix.

For patients, the impact remains mixed. On one hand, the presence of an authorized generic can lower out-of-pocket costs slightly compared to the brand. On the other hand, if the practice deters independent generic entry, the long-term savings from true generic competition are lost. The Congressional Budget Office estimated in 2012 that eliminating authorized generics during the exclusivity period could save Medicare $4.7 billion over ten years by encouraging more patent challenges.

Key Takeaways for Industry Professionals

If you work in pharmaceutical law, policy, or business development, here are the critical points to remember:

- Timing is Critical: Authorized generics launch fast. Expect them within weeks of a patent loss.

- Pricing Strategy Matters: They create a mid-tier price point that splits the market.

- Settlement Risks: Avoid agreements that explicitly restrict authorized generic entry. The FTC is actively investigating these.

- Small Markets are Vulnerable: For low-revenue drugs, the threat of an authorized generic may kill the incentive to challenge patents altogether.

- Monitor Legislation: Keep an eye on bills like the Preserve Access to Affordable Generics Act, which could ban these practices during exclusivity periods.

Are authorized generics legal?

Yes, authorized generics are currently legal in the United States. The Hatch-Waxman Act does not prohibit brand manufacturers from selling their own products under a generic label. The FDA considers them compliant because they are identical to the approved brand-name drug and require no new clinical trials.

How do authorized generics differ from traditional generics?

Traditional generics are manufactured by independent companies that must prove bioequivalence to the brand drug. Authorized generics are produced by the original brand manufacturer (or a licensee) and are physically identical to the brand product. They bypass the Paragraph IV patent challenge process and enter the market faster.

Why do the FTC and generic companies oppose authorized generics?

The FTC and generic companies argue that authorized generics undermine the 180-day exclusivity period granted to first-filing generics. By entering the market simultaneously, authorized generics capture significant market share and reduce the profits of independent generics. This reduces the incentive for generic companies to challenge patents, potentially keeping drug prices higher for longer.

Do authorized generics lower drug prices for consumers?

The impact is mixed. Authorized generics offer a price point lower than the brand but higher than independent generics. Some studies show they can lower on-invoice prices by 13-18%. However, critics argue that by discouraging independent generic entry, they prevent the deeper price reductions (often 80-90%) that occur when true generic competition emerges.

What is the future of authorized generics?

The use of authorized generics is declining due to increased FTC scrutiny and legislative efforts. While they are still projected to account for 20-25% of generic entries through 2028, their role in patent settlement negotiations is shrinking. Companies are moving away from using them as tools for anti-competitive agreements.