Imagine standing at the pharmacy counter, handing over your card for a medication you’ve relied on for years. The pharmacist frowns, types something in, and says, “This isn’t covered under your plan.” Or worse, “Your copay is $450 today.” It’s a scenario that plays out thousands of times every day. With 66.7% of adults in the United States using prescription drugs, understanding your coverage isn't just administrative busywork-it’s financial survival.

We often assume health insurance covers our meds because it’s called "health" insurance. But prescription drug coverage operates like a separate system within that system. If you don’t know the specific rules of your plan, you are essentially flying blind. This guide breaks down exactly what you need to ask your insurer or check on your policy documents before you buy your next pill.

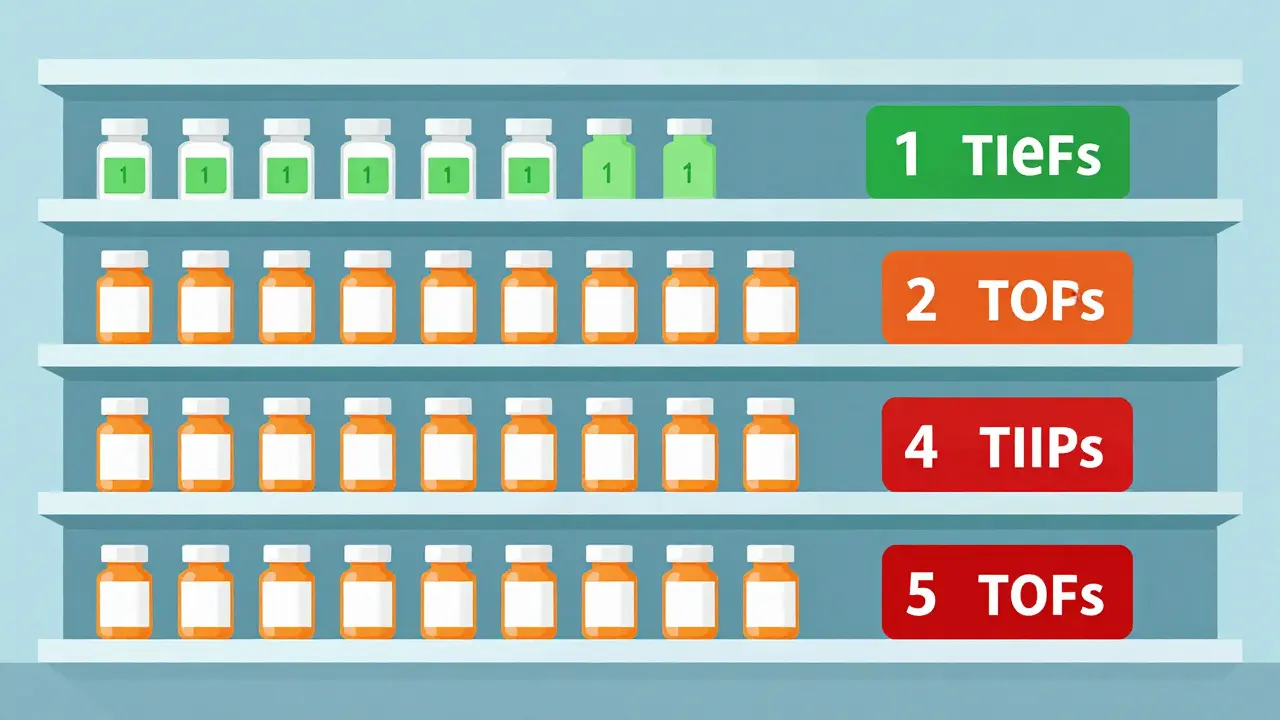

The Formulary: Your Plan’s Shopping List

The first thing you need to understand is the formulary. Think of this as your insurance plan’s approved shopping list. Not every drug exists on this list, and even if it does, where it sits on the list determines what you pay.

Most plans organize drugs into four tiers. Knowing which tier your medication falls into is the single most important factor in predicting your costs.

| Tier | Drug Type | Average Cost to You |

|---|---|---|

| Tier 1 | Generic drugs (e.g., Metformin, Lisinopril) | $10 - $20 copay |

| Tier 2 | Preferred brand-name drugs | $40 - $80 copay |

| Tier 3 | Non-preferred brand-name drugs | $100+ copay |

| Tier 4 | Specialty drugs (e.g., biologics for arthritis, cancer) | 25-33% coinsurance (often $1,000+) |

Ask your plan: “Is my specific medication on the formulary, and which tier is it in?” Don’t just ask if they cover "insulin"-ask about the exact brand and type you use. A generic might be Tier 1, while the brand name you prefer could be Tier 3, costing you ten times more per fill.

Deductibles and When Coverage Kicks In

Here is a trap many people fall into: assuming their insurance pays for prescriptions from day one. That is rarely true. Most plans have a deductible-a amount you must pay out-of-pocket before insurance starts sharing the cost.

If you have a Bronze Marketplace plan, your deductible might average around $6,000. Until you spend that $6,000 on covered services, you pay full price for everything, including generics. Gold plans, however, might have a deductible as low as $150.

You need to ask: “Do I have to meet my annual deductible before prescription coverage begins?” And follow up with: “Are any of my medications exempt from the deductible?” Some plans waive the deductible for Tier 1 generics but not for brand names. If you take expensive specialty drugs, hitting that deductible quickly is crucial, so knowing the threshold helps you budget.

Prior Authorization and Step Therapy

Even if a drug is on the formulary, your doctor can’t always just write the script. Two common hurdles are prior authorization and step therapy.

Prior authorization means your doctor must get permission from the insurance company before they prescribe the drug. They have to prove why you need it. About 28% of Medicare Part D prescriptions require this step. If your doctor forgets to do this, the pharmacy will reject the claim, and you’ll be stuck holding the bill.

Step therapy is stricter. It forces you to try cheaper, alternative medications first. Only if those fail can you move to the drug you want. This affects 37% of specialty drugs in some marketplace plans.

Ask your plan: “Does my medication require prior authorization or step therapy?” If yes, ask your doctor to start that paperwork immediately after your appointment. Do not wait until you need the refill.

Pharmacy Networks: Where You Fill Matters

Your insurance plan likely has a preferred network of pharmacies. Using an out-of-network pharmacy can spike your costs by 37% or more, according to consumer reports. For many plans, 78% limit coverage to specific networks.

This doesn’t just mean big chains like CVS or Walgreens. It might mean your local independent pharmacy isn’t in the network, or that mail-order options offer better rates for maintenance drugs.

Ask: “Which pharmacies are in-network for my plan?” Check if your preferred pharmacy is listed. Also ask: “Do I save money by using mail-order for 90-day supplies?” Many plans offer lower copays for mail-order refills of chronic condition medications.

Medicare Part D Specifics: The Gap and Caps

If you are on Medicare, the rules change slightly with new reforms taking effect in 2025 and beyond. Under the Inflation Reduction Act, there is now a hard cap on out-of-pocket costs for Medicare Part D beneficiaries starting in 2025.

Previously, there was a "donut hole"-a coverage gap where you paid 25% of drug costs between $5,030 and $8,000 in total spending. While this gap still technically exists in structure, the financial burden has shifted significantly. More importantly, monthly insulin costs are capped at $35.

Ask your Medicare plan: “What is my maximum out-of-pocket limit for 2026?” With the new caps, this number should be predictable. Also ask: “How does my plan handle the transition from the initial coverage period to catastrophic coverage?” Understanding when you hit that cap prevents surprise bills later in the year.

Plan Types: Bronze vs. Gold vs. Platinum

Choosing a plan isn’t just about the monthly premium. It’s about the actuarial value-the percentage of costs the plan pays versus what you pay. Bronze plans cover 60%, Silver 70%, Gold 80%, and Platinum 90%.

For someone who rarely sees a doctor, a Bronze plan with a high deductible looks cheap. But if you take regular prescriptions, that high deductible hurts. Data shows that someone filling 12 maintenance medications annually saves nearly $1,800 by choosing a Gold plan over a Bronze plan, despite the higher monthly premium.

Ask yourself and your advisor: “Based on my expected medication usage, which metal tier minimizes my total annual cost?” Look at the sum of premiums + deductibles + copays. Often, the "expensive" plan is actually the cheapest option for heavy medication users.

Specialty Drugs and High-Cost Medications

If you take specialty drugs-medications for complex conditions like cancer, rheumatoid arthritis, or multiple sclerosis-you face unique challenges. These drugs often cost over $100,000 a year. In 2023, half of all new FDA approvals were specialty medications.

Standard copays don’t apply here. You usually pay a percentage of the cost (coinsurance). Without proper coverage, these bills can be catastrophic.

Ask: “Does my plan have a special program for high-cost specialty drugs?” Many insurers have patient assistance programs or specialized care managers who help navigate coverage. Also ask: “Are there manufacturer copay cards accepted by my plan?” Sometimes combining insurance with manufacturer aid lowers your cost further.

When to Review Your Coverage

Coverage changes every year. Formularies shift, pharmacies drop out of networks, and tiers get adjusted. You shouldn’t wait until Open Enrollment to think about this if you notice a problem.

However, the best time to make changes is during specific windows:

- Marketplace Plans: November 1 - January 15 (Open Enrollment).

- Medicare: October 15 - December 7 (Annual Election Period).

During these times, use online tools. HealthCare.gov allows you to enter up to 15 medications and 3 pharmacies to compare plans side-by-side. Medicare’s Plan Finder requires NDC codes for precision. Spending just 20 minutes verifying your meds can save you over $1,000 a year.

Don’t guess. Call your insurer. Read the Summary of Benefits. Ask these questions directly. Your health depends on the medicine; your wallet depends on the answer.

What is the difference between a copay and coinsurance?

A copay is a fixed dollar amount you pay for a prescription, such as $10 or $40, regardless of the drug's actual price. Coinsurance is a percentage of the drug's cost that you pay, such as 20% or 30%. Copays are common for generic and preferred brand drugs (Tiers 1-3), while coinsurance is typically used for specialty drugs (Tier 4) where costs vary widely.

Can I appeal if my insurance denies coverage for a medication?

Yes. If your plan denies a prior authorization or places a drug in a higher tier than expected, you have the right to appeal. Your doctor can submit clinical notes explaining why the drug is medically necessary. Start with an internal appeal to the insurance company, and if that fails, you can request an external review by an independent third party.

Why is my generic drug not covered?

While rare, some plans may exclude certain generics due to contract issues with manufacturers or if they are deemed not medically necessary compared to alternatives. More commonly, a generic might be covered but require step therapy, meaning you must try a different, cheaper generic first. Check your formulary specifically for exclusions or restrictions.

How does the $2,000 out-of-pocket cap for Medicare work?

Starting in 2025, Medicare Part D beneficiaries will no longer face unlimited drug costs. Once your total out-of-pocket spending for covered drugs reaches $2,000 in a calendar year, the plan pays 100% of the remaining costs for the rest of the year. This cap includes deductibles, copays, and coinsurance.

Should I choose a PPO or HMO for prescription coverage?

PPOs generally offer more flexibility in choosing doctors and pharmacies, often with broader networks. HMOs usually have lower premiums but restrict you to in-network providers and pharmacies, and may require referrals for specialists who prescribe certain drugs. If you travel frequently or prefer specific out-of-network pharmacies, a PPO might be worth the higher cost.